|

If you have ever wondered what successful firms do, wonder no more. It’s a question that we have been asking ourselves since we began consulting, and after a combined 60 years of consulting, we believe we have the answers and want to share them with you.

We developed a list. Now, every firm is not perfect in each of these areas. But those firms that want to become the firm of choice in their chosen markets by moving up to the next level all focus on these activities. When you examine our list, determine where your firm would lie on a scale from 1 to 10, — 1 being that you are not doing the activity and 10 implying that you have solved the issue and your partners are aligned with it. We created a brief scoring at the end of the article. The important thing is figuring out what you need to do to get better and then starting your execution plan. Here’s our list of what the best firms do: 1. They have a clear vision and strategies for getting there. A vision without strategies is meaningless. We have found that in the best firms there is a shared understanding of what to do and shared commitment to achievement. These firms are not afraid to make tough people and market choices. And most importantly, the partners model the behavior needed to deliver sustained success. Your people and your partners will never change unless they see that the leaders start behaving differently. 2. They think about markets as well as clients. Markets today are constantly changing, and partners, who should be the first line of defense, need to continually scan the competitive environment. By doing this they can anticipate market changes and look for opportunities to enhance the firm’s service offering. With this intelligence the firm can decide what to do and what resources to invest in order to deliver the new offerings. 3. They develop a deep, deep client orientation. This is how they develop their brand name. Their reputation for delivering outstanding solutions precedes them. It’s all about providing solutions that are meaningful for the clients. If you do this, clients will actively seek you out. You will become part of the clients’ “institutional memory” and you will be the first port of call. 4. The firm’s people are as important as the firm’s clients. These firms have a reputation that it’s a hard place to be hired into, a hard place to be promoted, and a hard place to stay — but, when people move on, they do so as friends. In addition, the firm is committed to helping its people develop their expertise either inside or outside of the firm. Finally, the firm cares about its people, going out of its way to help with both work and personal situations. 5. They have a high-performance culture. Getting into these firms is not easy and when you do get in, everyone in the firm wants to be the best, to go the extra mile, and to seek new solutions that force competitors to react. 6. They have outstanding execution. These firms leverage ideas and expertise, regardless of their origin, to deliver client value. They focus on client solutions that are at the forefront of their thinking. Talking about something is not enough. It’s all about doing. 7. They embrace the one-firm concept. The partners put the firm before their personal interest. They realize that the team, not the individual, is what matters. Stars and lone wolves are downplayed. They believe and live an embedded set of principles and practices that maximize the trust and loyalty people feel for both the firm and their colleagues. 8. They have a strong culture and shared values. Their values are what hold the firm together, and if someone does not live the values, the firm is intolerant of wrong behavior. In these firms, the partners walk together. Yes, they disagree, but at the end of the day, they agree to agree. 9. They practice a highly collaborative style. People in these firms go out of their way to help each other. It’s not about me, but us. You can see this in the most successful firms because people have confidence in their colleagues to introduce them to their clients. 10. They have strong partnerships. In successful firms, partners see themselves as custodians of the firm’s future, creating an even better firm for the people who follow them. As we have said, the partners share and police the firm’s vision, values and strategies. 11. They have an absolute commitment to recruiting the right people. Not only do these firms recruit the right people, they get them into the right seats. Often the top partners lead the recruitment efforts. When they recruit, they recruit for cultural fit as well as technical competence. While qualifications are important, they focus on the individual. 12. They believe that developing their professionals is at the core of the firm’s beliefs and activities. Partners pass on their knowledge and expertise by actively coaching and mentoring. They realize that learning happens where the work gets done. 13. They are committed to staying at the top. These firms realize that they can never rest on their laurels. They are always looking for new ways to do things better. You may think that the above 13 items are overwhelming. No firm does everything 100 percent right. Even the “best of the best” are still working on areas. You might want to take one or two of the easiest things to improve upon. These are low-hanging fruit and will give you and your team some successes and confidence that you can start the change process. Start today! You will become a better firm with happier people. You have a great deal to gain if you go down this road and much to lose if you don’t. HOW DID YOU DO? The maximum score is 130. If you gave yourself this score, you might want to go back and re-examine your answers. All firms can improve in one or more areas. There will be only a handful of firms that have a score between 117 and 130. Several will fall in the 104-116 category, and the majority will be in the 91-103 group. Firms with a score of 90 or less should seek outside help and advice. Here’s how the scores break down: 117–130: Your firm is one of the best. Congratulations! 104–116: Your firm is moving in the right direction. You’re doing a good job! 91–103: Your firm is on the fence. Decide now which way you want to go. 78-90: Take the time now to get better. Get help! Below 78: Your firm needs help now! Robert Lees is a founding partner and director of Moller PSF Group Cambridge, and co-author of When Professionals Have to Lead. Reach him at [email protected]. August Aquila is CEO of Aquila Global Advisors, and co-author of Compensation as a Strategic Asset and Client at the Core. Reach him [email protected] or (952) 930-1295. Read Article: http://www.accountingtoday.com/news/firm-profession/the-secrets-of-their-success-79995-1.html  By now, you should be familiar with the cloud, but one question I get time and time again is how to choose a cloud vendor. With so many options, I agree it can be confusing. Here is some basic information to help you determine your needs, as well as a set of questions you can use to assess potential cloud vendors.

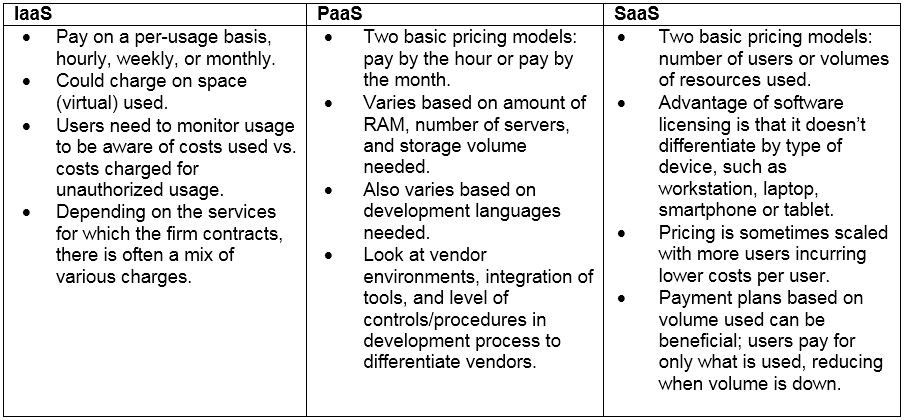

Types of vendors and services offeredFirst, decide how you are going to use the cloud. Depending on your organization's needs, you have to decide what service or services will help you reduce costs and increase efficiency and accessibility. The cloud comes in three flavors: infrastructure as a service (IaaS), platform as a service (PaaS), and the one you probably hear about most often, software as a service (SaaS). Let's take a quick look at what you need to know about each type of cloud offering. IaaS is the hardware and software that powers it all, including servers, storage, networks and operating systems.

PaaS is the set of tools and services designed to make coding and deploying those applications quick and efficient.

SaaS includes commercial applications designed for end-users and delivered over the web.

Questions to ask cloud vendorsDepending on your needs, you'll want to vet each cloud vendor through a careful, strategic review. Here is a comprehensive list of questions and observations in four areas. Stability of cloud vendors

Redundancy and availability

Customer service record

Security

All of the questions included above should not be considered an all-inclusive list to consider when choosing a cloud service vendor, but they are a good start. When companies are looking to outsource their information technology, they should perform a risk assessment and develop a project plan for transitioning to a cloud vendor. Finally, the project should be managed just like any other major project by monitoring progress during implementation; this helps to ensure the vendor is fulfilling the customer's needs as the agreement specifies. Good luck and may the cloud be with you. Read Entire Article: http://www.journalofaccountancy.com/newsletters/2016/nov/choosing-cloud-vendor.html They seem to be everywhere! I’ve seen them at trade shows and association meetings. They have been seen advertising in accounting profession journals and their promotional emails have probably reached your mailbox. They are making a lot of noise!

They are the vendors selling cloud accounting solutions. Are cloud accounting applications right for you and your clients? In this article, we’ll define cloud accounting and look at the risks and benefits. What is cloud accounting? Cloud accounting applications provide much of the same functionality as desktop accounting software with one major difference: Cloud accounting apps run on remote servers and are accessed via a web browser. Cloud accounting applications are typically offered in one of these two formats: Hosted applications – The hosted solutions involve your desktop or client/server accounting application running on a remote server. You gain access to your accounting software using a remote session via the Internet. This solution allows you to use your existing software and data. Software as a Service (SaaS) – In this format, the accounting software and your data are stored on the vendor’s servers and are accessible via a web browser. If you have ever used a social media site or online banking, you have used a SaaS solution. What are the benefits? There are numerous benefits to cloud accounting and progressive business owners are enjoying them. Here are a few of the benefits: Anytime, anywhere access – Your accounting software and operating results are available to you from a browser or mobile device. This is something that you can’t do with today’s desktop accounting solutions. Better security – Most cloud accounting software is run from a data center, which offers multiple levels of security to protect the software and your data. The typical data center has significantly better security than most small businesses. No installations or updates required – Cloud accounting vendors maintain the software and install the updates. Automatic backups – The cloud vendor assumes responsibility for system backups. Your data is often stored in multiple data centers that are in geographically diverse locations. No startup costs or long-term commitments – Cloud accounting applications are rented not purchased. They do not require a small business to invest in servers or software. Platform agnostic – Do you prefer a Windows PC or Mac? What’s your choice, Chrome, Internet Explorer or Firefox? In the world of cloud accounting, it simply doesn’t matter. Cloud accounting applications are delivered via a web browser and typically support all popular platforms. What are the risks? The world of cloud accounting is not without risk. These solutions are new and require that you perform the necessary due diligence to determine if the solution is right for your business. Here are a few of the risks: The vendor goes away – Over a decade ago, we experienced a tech bubble where vendors were here one day and gone the next. The same risk exists with cloud accounting vendors. It is important to have a contingency plan. You don’t have Internet access – Cloud accounting vendors are accessible from anywhere and anytime assuming that you have a connection to the Internet. If you find yourself without internet access, you will not have access to your accounting data. Security breach – Cloud accounting software and your data both live on the Internet. There is a risk that someone could gain access to your data. What’s next? We are just beginning to see the impact of cloud accounting applications. It will take time to determine if they will be the next major paradigm shift in the world of accounting. There is so much more to learn about these products and their impact on the small business community. Stay tuned! Read Article: https://www.firmofthefuture.com/content/cloud-computing-benefits-and-risks-of-cloud-accounting/  The Consumer Protection Financial Bureau recently published guides to help those who are managing someone else's money, specifically those who have power of attorney; those appointed by a court as guardians or conservators of property to manage money and property for someone who cannot manage it alone; trustees under revocable living trusts, and those appointed by a government agency to manage someone else's income benefits like Social Security.

"Fiduciaries are generally expected to act in the other person's best interest, manage their finances carefully, keep those finances separate from their own, and maintain good records," CPFB Director Richard Cordray said in a prepared statement when the guides were published. Here's how to do the best job possible if you're asked to help out. Get a clear picture of their finances When managing an elderly person's money, it is important to have a sit down with that person to go over all of their expenses and establish a budget, says Leslie Tayne, an attorney with the Tayne Law Group, specializing in financial issues. "The budget should include room for additional funds in case of emergencies." Carla Blair-Gamblian, a credit expert for Veterans United Home Loans, says to set the budget to live off as little as possible. "Leave funds in savings and try to live off pension, annuities and Social Security monthly payments. Retirees and the elderly need to maintain as much capital as possible so they have money for emergencies." Then too, she says that money in savings can build interest and ensure some additional cash flow and growth. "Regularly check your loved one's credit and put a credit lock on, so no one can take out credit in their name" -Leslie Tayne If upon review you find there is more month than money, you'll have to look for ways to reduce their expenses. "Think outside the box in terms of what the right solution might be for the senior in your life," says Dan White, founder and president of Daniel a. White & Associates. "Maybe they haven't considered downsizing or moving closer to other family members who can help provide care. Communication is critical for these tough decisions, but the right moves can improve quality of life for everyone involved." If the senior is not capable of discussing what bills they are responsible for, when they are due, and how much they owe, dig on your own on their behalf by sorting through mail and reviewing bank statements to see what bills are paid regularly. "Contact all of their bill companies' and ask that they mail and/or email all copies of the bills to your mailing and/or email address," says Tayne. Consider being an authorized user on all bank accounts. Do set minimum balance alerts so you will be informed when the balances fall below a certain point. This is also a good way to keep track of purchases and to monitor accounts for any suspicious activity like identity theft. "Regularly check your loved one's credit and put a credit lock on, so no one can take out credit in their name," she adds. Keep an eye out for signs of fraud and abuseThe elderly are often the target of scammers. "I have had clients who have received fraudulent emails or phone calls regarding their bills, health insurance, Social Security, etc.," says ReKeithen Miller, a certified financial planner with Palisades Hudson Financial Group. Given the possibilities, it's a good idea for you to have your loved one consult you before they respond to letters and email they receive, and to tell them to politely decline when they get calls for solicitations. If your loved one sees something on one of those infomercials that they just must have, suggest that they write the phone number down and that item can be researched by you before they buy it, says Melody Juge, founder and managing director of Life Income Management. What you need to know Do know that problems can arise if you want to make payments and your name is not listed on the accounts. Realize too, that becoming a user or co-account holder on any accounts could potentially affect your credit score. Set reminders so you ensure that you don't forget to pay bills, as a missed payment could put you and your loved one's credit scores at risk. You can also automate payments. Makes sure though, that accounts are set up in a way that protects your loved one's assets from your creditors. "Think about what happens if you are sued, if their assets are in your name or if you share an account, you could inadvertently put your loved one's assets at risk," explains Mitch Adel, senior partner, and certified elder law attorney with Cooper Adel & Associates. "Under no circumstances should you commingle funds", says Blair-Gamblian. Clear records will settle any issues and answer questions family members might have about how the money is being managed. Avoid cash transactions which could become difficult to explain as well. "Do not make a personal loan or give yourself gifts from their money," advises Steve Starnes, a financial advisor with Savant Capital Management. Without a properly drafted power of attorney or trust, you will not have the authority to take action on behalf of your loved one. Worse, says Adel, you may have no way to help them protect their assets in the event of a catastrophic health care problem that may require them to spend down their assets. The best advice says Adel, "Plan before you have a crisis. Ask for counsel from a certified elder law attorney. This will ensure that your loved one's wishes and priorities are clearly identified, so you have the knowledge, tools and support you need to succeed as their helper." Read Article: https://www.depositaccounts.com/blog/how-to-manage-your-elderly-loved-ones-money.html  Written by Allan Branch

We have the smartest and most clever accountant in the world. So we asked him to give us some accounting tips for small businesses just starting out. Here’s what he wrote. It’s solid advice from an accountant who saves us tons of money. If you want a referal to our personal accountant just let me know in the comments. Accounting Tips

General Small Business Tips And Advice

Read Original Article: https://lessaccounting.com/blog/accounting-tips-for-small-businesses/#  The Internal Revenue Service is looking for information on bitcoin users from Coinbase, one of the largest bitcoin exchanges in the U.S., as part of its efforts to uncover possible tax evasion.

The IRS sent a broad request known as a John Doe summons to Coinbase last week seeking information on all of the San Francisco-based service’s users, according to The New York Times. The request follows on the heels of a report earlier this month from the Treasury Inspector General for Tax Administration that found the IRS should be doing more to ensure taxpayers aren’t using virtual currencies like bitcoin to avoid taxes (see IRS Warned to Safeguard Against Illegal Use of Virtual Currency). The IRS did not immediately respond to a request for comment. However, the IRS filed an affidavit with the court last Thursday explaining its request, according to the technology website Ars Technica. “The information and experience of the IRS suggests that many unknown US taxpayers engage in virtual currency transactions or structures... Because the IRS does not know the identity of the individuals within the ‘John Doe’ class, the IRS cannot yet examine the income tax returns filed by those US taxpayers to determine whether they have properly reported any income attributable to virtual currencies.” The company plans to challenge the IRS’s request for information on its customers. Coinbase spokesman David Farmer directed Accounting Today to a comment posted on its blog last Friday about the IRS request. “Our customers may be aware that the U.S. government filed a civil petition yesterday in federal court seeking disclosure of all Coinbase U.S. customers' records over a three year period. The government has not alleged any wrongdoing on the part of Coinbase and its petition is predicated on sweeping statements that taxpayers may use virtual currency to evade taxes. Although Coinbase's general practice is to cooperate with properly targeted law enforcement inquiries, we are extremely concerned with the indiscriminate breadth of the government's request. Our customers’ privacy rights are important to us and our legal team is in the process of examining the government's petition. In its current form, we will oppose the government’s petition in court. We will continue to keep our customers informed on developments in this matter.” Read Article: http://www.accountingtoday.com/news/tax-practice/irs-seeks-information-on-bitcoin-users-from-coinbase-79920-1.html The IRS will likely begin accepting income tax returns in the upcoming filing season with “no significant delays,” IRS Commissioner John Koskinen told the AICPA National Tax Conference in Washington on Tuesday.

Return filing can begin “certainly before the end of January,” Koskinen said, although he did not announce an exact date. The IRS’s ability to start tax season on time partly reflects that the current run-up to tax season, unlike previous ones, is not hampered by uncertainty surrounding the fate of the retroactive extension of expired tax provisions, thanks to the Protecting Americans From Tax Hikes (PATH) Act of 2015 (part of the Consolidated Appropriations Act, 2016, P.L. 114-113). However, for some taxpayers, Koskinen said, the PATH Act will mean delays in receiving refunds. Due to a change to Sec. 6402(m), starting in 2017, refunds for returns claiming an earned income tax credit or additional child tax credit cannot be issued before Feb. 15. Despite this statutorily mandated delay, Koskinen urged return preparers to submit returns as they usually do, and not hold them until after Feb. 15, because that will only put the returns further back in the queue. Security measures Another new PATH Act change for 2017 requires Forms W-2, Wage and Tax Statement, to be filed with the Social Security Administration by Jan. 31. Those changes are intended to give the IRS a better chance to check returns and prevent improper payments and better protect taxpayers against fraudulent refund claims using stolen identities, Koskinen noted. Koskinen said he hoped the Service could build on a successful 2016 filing season that saw improved levels of telephone service to taxpayers and practitioners, and progress throughout the year in stopping identity theft fraud. The former, he said, was largely due to an additional $290 million funding appropriation. The IRS’s need for increased funds after years of budget cuts was a constant refrain through Koskinen’s address, and he said it will be his biggest priority in the remaining year of his five-year term as commissioner. Koskinen touted the work this year of the Security Summit, a cooperative effort by the IRS with representatives of preparers, the tax preparation software industry, financial institutions, and state tax administrators, noting that its work accompanies a drop of more than 50% in filings by taxpayers of Form 14039, Identity Theft Affidavit. But, he said, thieves may be adapting. Foreign organized crime syndicates have a “stunning” estimated 1 billion stolen online user IDs and passwords with which to “ping” banks for financial account access. “It’s no longer beanbag we’re playing here,” he said, “but a serious, ongoing battle.” In trying to predict thieves’ strategy, the IRS has grown increasingly concerned about tax preparers’ systems and their vulnerabilities. “If they can hack into your systems and get the data about your clients, they are better able to file a more effective-looking fraudulent return,” he said; hence the IRS is promoting its “Protect Your Clients; Protect Yourself” campaign. Another security measure Koskinen promoted for the upcoming filing season is expansion of the use of a 16-digit verification code on Forms W-2 from 2 million last year to 50 million, and he urged practitioners in the audience to enter any such code they encounter into returns. This could help reduce the number of false positives in the millions of suspicious returns the IRS stopped last year. IRS future state Koskinen also sought to reassure the audience that the IRS’s Future State initiative would not require taxpayers who do not wish to interact with the IRS online to do so but would allow them to communicate by phone or in person. Earlier Tuesday, National Taxpayer Advocate Nina Olson described her reservations on that score. Olson said she has observed in recent years that “as the responsibilities of taxpayers have become more and more onerous, the IRS has become more remote.” She identified her top priority going forward as working to encourage a culture of engagement by the IRS with taxpayers and one not as quick to assume taxpayers are not complying with their obligations. The IRS’s primary goal should be “building trust, not just by creating an online account by which they can look up what they owe,” Olson said. Koskinen stressed that the Future State is “not some new invention” but part of a natural evolution in recent years of online tools such as “Where’s My Refund?” and online installment agreements—for taxpayers who prefer to deal with the IRS online. And having more taxpayers get their answers online could in turn improve the IRS’s telephone service, as well as allowing for quicker review of returns for errors that taxpayers can correct more expeditiously and simply, he said. See more at: http://www.journalofaccountancy.com/news/2016/nov/no-delays-anticipated-in-2017-tax-filing-season-201615547.html#sthash.x2UcfzA5.dpuf  The steps you take to starting a practice are fairly straight-forward: You apply for business licenses, find some affordable office space, come up with a snappy name for your practice, and sign your first client. But launching an accounting practice is only half the battle. Next, you work long and hard hours, building your client base bit by bit and then it happens: you hit a brick wall. You can’t add on more clients without adding overhead, and when you add more overhead, it eats into your already thin margins.

This isn’t necessarily a cause for concern. After all, your bills are getting paid and your current clients are happy. But at the end of the day, when you look at your MOM revenue and see a thick, flat line, you just aren’t satisfied. You know in your heart that greatness is within your reach, you just aren’t quite sure how to get there. Well, we’ll tell you all about the three simple ways any practice can grow their business on even the tightest of budgets. Examine Your Current Client Base First, ask yourself three simple questions: Do I know why our clients chose us? Do I know why they stick with us? And, do I know what our clients need going forward? These fundamental questions are too often taken for granted. The first two in particular are often waved away with a curt answer: “Because we’re great at what we do.” While that may be true, competency is not a defensible position. Competency is table stakes. If you want to scale your business, you need to determine what makes your practice different and what you can promise that your competition can’t. Maybe it’s technology. Maybe it’s price. Maybe it’s your bedside manner. Maybe (and hopefully) it’s because of some great, proprietary process you have in place. The point is, it’s almost always not simply because you’re keeping their books balanced and whatever that reason is, that’s a core quality you should focus on in your pitch to new clients. Answering the third question is much more difficult to answer, but also orders of magnitude more important. Having an open and ongoing dialog with your clients is beneficial for many reasons, but the most relevant to this topic is the ability to determine which services you should prioritize adding to your practice’s offering. For example, outsource CFO services are a big trend in today’s marketplace, but if your existing clientele lets you know that ensuring compliance is hot on their minds, you might invest in better auditing capabilities to grow your current client billables before hiring on a financial advisor to try and chase down new leads. These three simple questions will give you a starting point for determining the right way to market your business and finding the new revenue you need to grow. Efficiency is Everything Time is a resource that must be managed well in order to achieve scale, and it’s important that we recognize that. Too much time? You end up with a cadre of accounts who are burning hours on things that don’t bring in money. Too little time? You either have to increase overhead by bringing in additional people or overwork your employees and increase the risk of a mistake being made. Many practices make the mistake of trying to find that balance of resources through new business, when you really a lot of resources can be freed up by implementing new processes. Think about it this way: Say you want to grow your business of a 100 clients by 10%. From a new business perspective that means you need to sign 10 new clients and consider hiring on a new CPA to handle the increased workload. Taking a process oriented approach, you instead look for ways to cut down on the time it takes to deliver services. If you cut the time it takes to service a client from end-to-end by 10%, the extra margin you make on servicing your existing clients is nearly equal to the profit gain you’d make from adding on 10 clients under the old model. But that’s not all. By increasing efficiency in your operations, you’ve also increased your existing workforce’s capacity by 10%. This means you can still go out and add on those 10 new clients, only this time, you won’t need to add to headcount to service them. Finding and implementing more efficient processes is the best way to unlock profit potential. It’s not just a good idea, it’s probably the most critical component to taking your business to the next level. When you work smarter and not harder, you better believe it pays. Leverage New Technology Since the invention of the wheel, added efficiency has been the primary driver of technology adoption. Today is no different. It’s no secret that the accounting industry in the US skews conservative, but being bearish on technology often means money left on the table. There are countless case studies of more technologically advanced firms in the UK and Australia accelerating the growth of their businesses by readily and eagerly embracing new tools. And even in the US, we are seeing pioneering firms outpace more conservative firms thanks in part to their use of new technology designed to make their business hum. The first step to unlocking efficiency is switching away from desktop software and starting to use cloud-based software like QuickBooks Online or Xero. That’s a big first step, and you don’t have to tackle it all at once. In fact, it’s typically recommended that you migrate a small handful of clients to cloud systems at first until you can familiarize yourself with the software and how it works. Once you start working in the cloud, you’ll notice a number of small things that make servicing clients more efficient. Things like automatic bank reconciliation, a single ledger system that keeps the clients and your CPAs on the same page, and powerful web-based reporting that makes generating PowerPoint and Excel reports a thing of the past. The most powerful element of cloud based accounting tools are the API. Without getting overly technical, the API allows other tools to communicate with your accounting software and share data. Tools like Receipt Bank, advanced accounting automation software that helps you streamlines bookkeeping by automatically extracting valuable financial data from client submitted receipts and invoices. Customers who use Receipt Bank save dozens if not hundreds of hours per month on bookkeeping by letting the software do the legwork and having their accountants focus on the client. Read Article: http://www.accountingtoday.com/partner_insights/articles/3-ways-to-scale-your-practice-on-a-shoestring-budget-79413-1.html The Internal Revenue Service’s Office of Professional Responsibility has created a new online lookup table that allows the public to find out more easily if they have hired a rogue tax practitioner.

The new disciplinary look-up tool is basically just a Microsoft Excel file, but it includes searchable information about practitioners who have been censured for Circular 230 misconduct or received suspensions and disbarment from practicing before the IRS for the past 25 years. “Currently, members of the public can only learn that a practitioner was sanctioned by reviewing each of the announcements of discipline published in the Internal Revenue Bulletin on irs.gov, or by using a commercial subscription service (such as Tax Notes Today) that reports instances of Circular 230 discipline,” said the Office of Professional Responsibility in an email Wednesday. “The OPR’s solution is to compile the information into a searchable Excel document file.” The list includes basic information from the past 25 years on more than 3,000 censures, suspensions, disbarments and other restrictions on practitioners. Examples include permanent injunctions and denials of limited practice to unenrolled tax return preparers due to misconduct. The IRS’s OPR plans to keep the document up to date with any new entries whenever a disciplinary announcement is published in the Internal Revenue Bulletin. The OPR will also update the information to reflect when a tax preparer has been reinstated to practice before the IRS after the end of a practitioner’s suspension or disbarment, and to remove any data related to a disciplinary sanction once the date it was imposed passes the 25-year mark for the OPR’s record retention requirement. The list includes the last name, first name, and middle initial (if applicable) of tax practitioners, along with the city, state, designation, disciplinary sanction, effective date, and ending date (when the practitioner is now in good standing and may represent taxpayers before the Service). The spreadsheet can be searched using the “Sort & Filter” and “Find & Select” features. Read Article: http://www.accountingtoday.com/news/tax-practice/irs-makes-it-easier-to-look-up-disciplinary-records-of-tax-practitioners-79891-1.html  There’s no shortage of details to consider when you’re a small business owner. Getting the back-office basics of accounting in order early on – tracking revenues, expenses and costs – will keep you out of the weeds of paperwork and cash flow snafus, and onto the important work of growing your business.

“You can get away with doing your own bookkeeping and accounting when you first start out,” says New York-based CPA Maggie Kirkendall. “But once you’re ready to file tax returns you often realize you didn’t know enough, or didn’t want to spend enough time to figure it out, and that’s when I suggest getting a bookkeeping or accounting service to help you maximize any tax advantages.” Fees can be “atrocious,” she concedes, so in the meantime consider automating your small business accounting with one of the many finance software applications available to you, such as Xero, QuickBooks, FreshBooks or Wave. Go with the software that best suits your needs, like having cloud-based access or user-friendly iPad apps. Bookkeeping is a necessary chore of all businesses, helping you manage your operations and prevent an audit by giving the IRS what they need. To keep moving toward your long-term goals and improve profits, get your small business accounting in order with these essential tips:

Read Article: https://www.fundera.com/blog/2014/06/16/9-tips-get-small-business-accounting-order |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

September 2017

Categories |

RSS Feed

RSS Feed